Quick Answer: What is the difference between whole and term life insurance?

- Term life insurance provides coverage for a specific period, like 10 to 30 years, and pays a death benefit only if you die during that term.

- Whole life insurance provides lifelong coverage and includes a cash value component that grows over time.

- Term is affordable and simple, while whole life is more expensive but builds permanent financial equity.

Choosing the right policy protects your family’s financial future. At Zoellner Insurance, we help clients across Tulsa and surrounds navigate their options every day. This guide breaks down the choice between term life and whole life insurance. We focus on the specific needs of residents in Tulsa, Broken Arrow, Jenks, and surrounding communities.

What Is Term Life Insurance?

How does term life insurance protect your family?

Term life insurance covers you for a set number of years. You select a period – such as 10, 20, or 30 years – that matches your longest financial responsibilities. If you pass away during this timeframe, the policy pays a tax-free cash death benefit to your beneficiaries. If the term ends, the coverage stops completely unless you renew it.

Who is Term Life Insurance Best For?

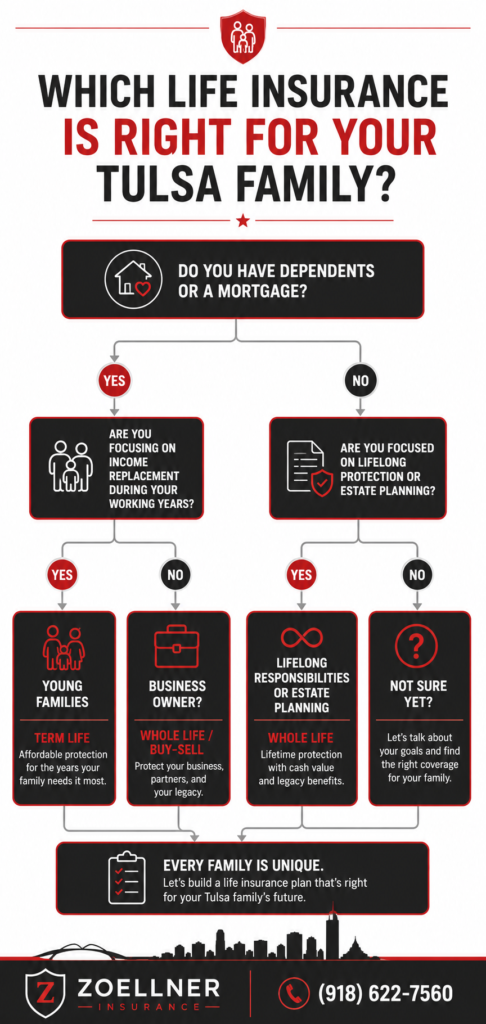

Young families in the Tulsa area often choose term life insurance. It provides large amounts of coverage for a low monthly cost.

For example, a young couple buying a home in Broken Arrow might select a 30-year term policy. The policy matches the length of their mortgage. If one parent passes away, the payout ensures the surviving spouse can pay off the house.

Parents also buy term insurance to protect their children until they reach adulthood. A 20-year term policy covers a newborn until college graduation. The funds can replace income, pay for child care, or cover tuition at local institutions like the University of Tulsa.

How are Term Life Insurance Premiums Structured?

Term life insurance operates on a level-premium system. This system ensures your monthly payment remains identical from the first day of the policy to the last day of the chosen term. Insurance companies calculate these premiums based primarily on your age, health history, and lifestyle choices at the time of your application.

Why Do You Actually Need Term Life Insurance?

Term life insurance functions strictly as an indemnity product. It does not contain investment features or equity accounts. Because you pay solely for pure death protection, the monthly premiums remain highly cost-effective. This affordability allows families to secure large face amounts of coverage without straining their monthly cash flow.

What Is Whole Life Insurance?

How Does Whole Life Insurance Accumulate Value?

Whole life insurance stays active for your entire lifespan, provided you pay the required premiums. Unlike term policies, whole life combines a permanent death benefit with a tax-deferred savings component known as cash value. A portion of every premium payment builds equity within the policy, which you can access or borrow against during your lifetime.

As your cash value grows, it becomes a powerful financial tool. You can take out a policy loan against this equity to fund opportunities, such as expanding a small business in downtown Jenks or paying college tuition at the University of Tulsa. These loans do not require credit checks, and you do not face a rigid repayment schedule. However, any outstanding loan balances reduce the final death benefit if you pass away before repaying the debt.

Who is Whole Life Insurance Best For?

Whole life insurance appeals to individuals and families who want permanent protection. It suits individuals with lifelong financial responsibilities.

For instance, parents of children with special needs use whole life insurance. They must secure funds that support their child long after the parents pass away. A term policy does not fit this scenario because the term might end too soon.

Business owners in Jenks or Owasso also utilize whole life insurance for succession planning. They use the permanent death benefit to fund buy-sell agreements. This cash ensures a smooth transition of business ownership.

High-net-worth individuals in Tulsa look at whole life insurance for estate planning. The permanent payout can cover estate taxes or help divide an inheritance equally among heirs.

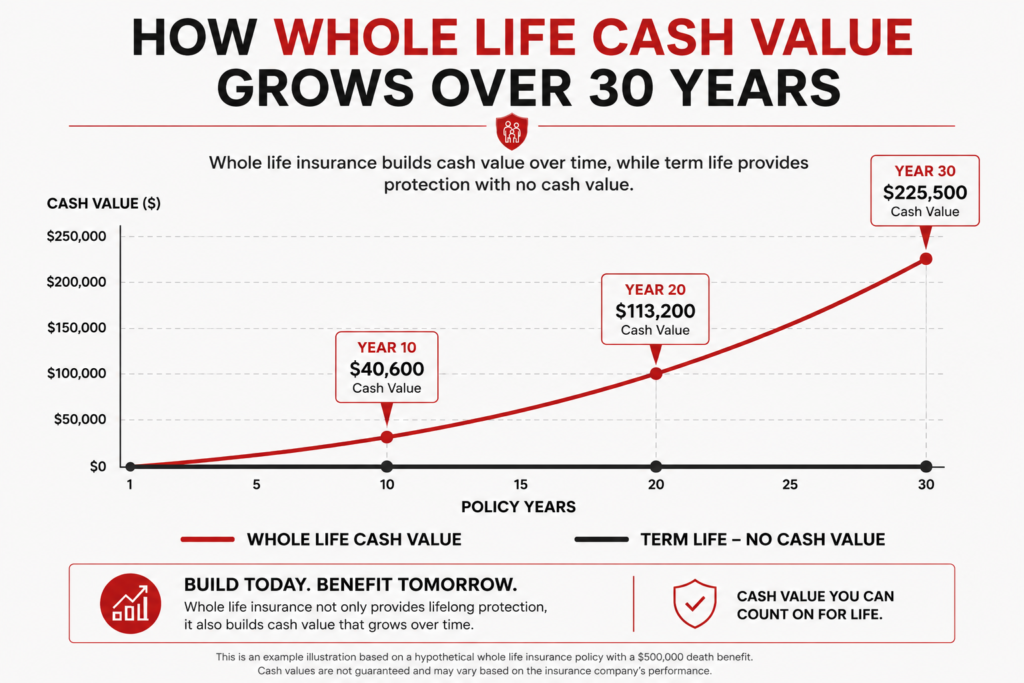

Understanding the Cash Value of Whole Life Insurance

Whole life premiums remain level for life, but they cost significantly more than term premiums. In the early years of the policy, your premium payment exceeds the actual cost of insuring your life. The insurance company channels this excess money into your policy’s cash value account. This account grows at a guaranteed minimum interest rate set by the carrier.

Participating vs. Non-Participating Policies

When selecting whole life insurance, you choose between participating and non-participating structures. Non-participating policies offer standard, guaranteed growth with predictable cash values and fixed death benefits. Participating policies allow you to earn annual dividends from the insurance provider.

While insurance companies do not guarantee dividends, established mutual carriers routinely distribute them. You can use these dividends in several ways:

- Cash payouts: Receive a direct check from the carrier.

- Premium reduction: Apply the funds to lower your next monthly payment.

- Paid-up additions: Buy extra mini-policies to increase your total death benefit and accelerate cash value accumulation.

What Are the Key Differences Between Term and Whole Life Insurance?

The structural differences between these two options alter your premium costs and financial outcomes. The table below outlines how each policy type handles duration, equity, and cost adjustments.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Policy Length | Specific period (10 to 30 years) | Your entire lifetime |

| Premium Cost | Lower initial cost | Higher initial cost |

| Premium Stability | Stays flat for the term | Stays flat for life |

| Cash Value Feature | None | Grows over time |

| Main Purpose | Income replacement, debt payoff | Permanent protection, wealth transfer |

How Do You Choose Between Term and Whole Life Insurance?

Your current financial stage dictates your insurance needs. You must look at your budget and your long-term goals.

Assess Your Budget

Term life insurance fits tight budgets. The premiums are significantly lower than whole life premiums for the same death benefit amount. If you need maximum coverage right now but have limited cash, term insurance solves the problem.

Whole life insurance requires a larger monthly commitment. You pay for the permanent guarantee and the cash value accumulation. Ensure your income can sustain the higher premium over the long haul. Dropping a whole life policy early can cause financial loss.

Look at Your Debts

Match your life insurance to your debt structure. Tulsa area home prices vary by neighborhood. A large mortgage in Bixby demands strong protection.

If your primary goal is covering a 20-year or 30-year mortgage, term life insurance matches that timeline perfectly. You pay for coverage during your peak debt years. Once you pay off your debts and your children leave the nest, your need for large insurance amounts drops.

Plan Your Legacy

Consider what you want to leave behind. If you want to guarantee a payout to your heirs, grandchildren, or a local charity, choose whole life insurance. It removes the risk of outliving your policy. The cash value component also serves as an emergency asset source during your retirement years.

Why Does Your Location in the Tulsa Area Matter for Life Insurance?

Local factors influence how much coverage you require. The cost of living in Oklahoma is lower than the national average, but regional costs still drive financial needs.

Housing and Income Factors

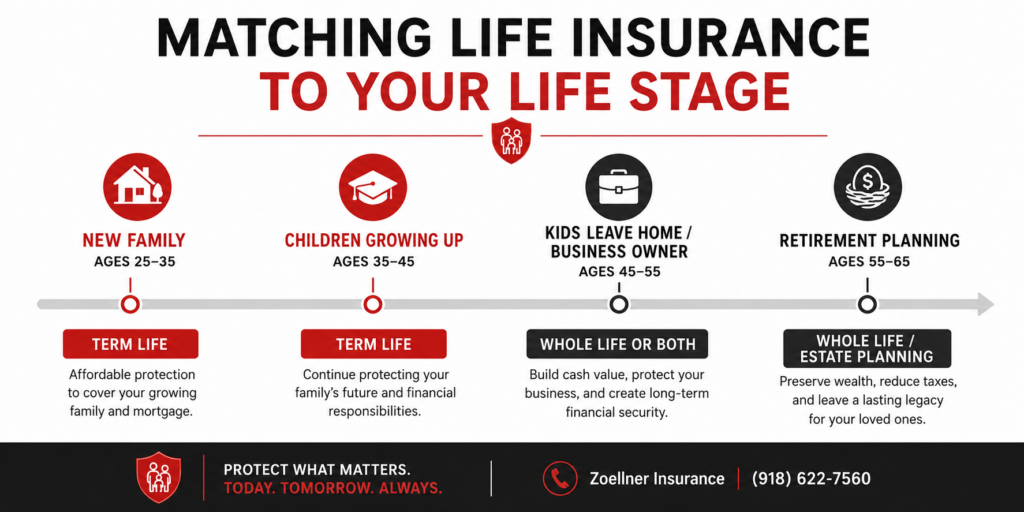

The Tulsa metro area features diverse housing markets that require distinct insurance approaches. Suburban expansion in Bixby and Owasso has led to an influx of young families purchasing larger homes. For these households, term life insurance serves as an ideal safeguard. A 20-year or 30-year term policy matches the timeline of suburban home ownership, shielding families from mortgage default during their high-expense years.

Conversely, historic neighborhoods in midtown Tulsa often attract established professionals or generational residents. Homes here frequently carry smaller mortgages or are owned outright. In these scenarios, the need for long-term mortgage protection decreases, opening the door for permanent financial planning strategies.

Local Business Protection

Tulsa has a thriving small business community. From retail shops in the Blue Dome District to manufacturing firms in Catoosa, local business owners face unique risks.

If you own a business, your life insurance does more than protect your home. It protects your business partners and employees. We recommend looking into how life insurance in Tulsa OK can safeguard your business equity.

Permanent policies can keep a local company afloat during a leadership crisis. Local business owners make use of whole life insurance for business continuity planning. A specific strategy called a buy-sell agreement often utilizes permanent life insurance.

In a buy-sell agreement, business partners purchase policies on each other. If one partner passes away, the surviving partner uses the tax-free death benefit to buy out the deceased partner’s shares from their heirs. The guaranteed cash value growth within a whole life policy also acts as an asset on the company’s balance sheet, providing emergency capital that stabilizes corporate cash flow during local economic downturns.

Oklahoma Estate and Probate Realities

Oklahoma probate law can involve lengthy court processes and administrative costs for families settling an estate. Life insurance death benefits bypass the probate court system entirely. The insurance company pays the funds directly to your named beneficiaries, usually within a few weeks of receiving the death certificate.

For wealthy families in the Tulsa area, whole life insurance provides the necessary liquid cash to pay potential state taxes, final medical bills, and legal fees. This liquidity prevents heirs from forcing a quick sale of family land, ranching operations, or local real estate assets to cover immediate debts.

What Riders Can You Add to Your Life Insurance Policy?

Riders are optional add-ons that customize your coverage. Both term and whole life policies accept riders.

- Waiver of Premium: This rider pauses your premium payments if you suffer a serious disability and cannot work. It keeps your policy active while you recover.

- Accelerated Death Benefit: This option allows you to access a portion of your death benefit during your lifetime if a doctor diagnoses you with a terminal illness. You can use the funds for medical treatments or comfort care.

- Child Term Rider: This rider adds small amounts of life insurance protection for your children. It covers funeral costs if an unexpected tragedy occurs.

Ask your agent about available riders during your consultation. Choosing the right riders adds extra layers of safety to your basic plan.

When to Select Term Life Insurance

Term life insurance fits households focused on maximizing immediate protection while controlling costs. Consider term insurance if you meet the following criteria:

- You need to replace your income during your working years to protect your children.

- Your primary goal is paying off specific debts, like a home mortgage or student loans.

- Your current monthly budget requires affordable premium payments.

- You prefer to invest your extra capital in separate vehicles, like employer-sponsored 401(k) plans or IRAs.

When to Select Whole Life Insurance

Whole life insurance fits individuals looking for lifelong coverage and integrated financial growth. Consider whole life insurance if you meet the following criteria:

- You want to guarantee that your beneficiaries receive a death benefit, regardless of when you pass away.

- You want a conservative, low-risk asset that accumulates guaranteed cash value over time.

- You need to fund a permanent obligation, such as caring for a dependent child with special needs.

- You want to build a pool of liquid capital for estate planning or business succession.

Frequently Asked Questions

Many term life policies include a conversion rider. This feature allows you to change your term policy into a whole life policy without taking a new medical exam.

This option protects your insurability. If you develop a health condition during your term, you can still secure permanent coverage. You convert the policy based on your original health status, though your premium will increase to match the whole life rates for your current age.

Young professionals often use this strategy. They start with affordable term insurance. As their income grows in their 30s and 40s, they convert portions of that term coverage into permanent whole life insurance.

Yes. Many people use a ladder strategy. They buy a whole life policy for permanent needs, like funeral expenses. Then, they add a term policy to cover temporary risks, like their mortgage or child-raising years.

For term insurance, the policy cancels, and your coverage ends. For whole life insurance, you may have options. The company can use the accumulated cash value to pay the premiums, or you can take the cash value amount and end the policy.

Yes. Oklahoma state statutes generally protect life insurance death benefits from the creditors of the insured person. The money goes directly to your named beneficiaries to secure their welfare.

Review your policy every three to five years. You should also check your coverage after major life events. These events include marriage, the birth of a child, purchasing a home in the Tulsa area, or starting a business.

The Oklahoma Insurance Department enforces strict consumer protection regulations on all life insurance carriers operating in the state. Oklahoma law provides a standard 10-day “free look” period. This period allows you to review your newly issued policy and return it for a full premium refund if you change your mind. The state also mandates a 30-day grace period for missed premium payments before a policy cancels.

No. The cash value inside a whole life policy grows on a tax-deferred basis. You do not pay annual income taxes on the interest or dividends your policy accumulates. If you withdraw cash from the policy, you only pay taxes on the amount that exceeds the total premiums you paid into the policy. Policy loans remain completely tax-free as long as the policy stays active.

If you can no longer pay your whole life premiums, you have several non-forfeiture options. You can surrender the policy entirely and receive the accumulated cash value minus any carrier fees. Alternatively, you can use the cash value to execute a “reduced paid-up” policy. This option stops your premium payments and changes your policy into a permanent one with a smaller death benefit. You can also use the equity to buy an extended term policy for a set number of years.